BMTC Group

A smaller Leon's-like opportunity with more question marks

It’s always nice to be able to re-use work you’ve done on a company to apply it to another in the same industry.

I’m going to do that with furniture stores.

Thank you to all who read and enjoyed my post on Leon’s. It was fun to write and learn more about the company as it is an iconic brand in Canada, and the furniture industry in this country. One of the responses to the post I saw on Twitter came from Gus Martin, who I have to thank for bringing BMTC back to my attention.

Years ago, friend of the Substack Nikhil fairly often brought up BMTC to me. At the time I was a dumber investor, so I’d look at the stock, maybe look at the revenue growth and P/E or whatever, and dismiss the idea…

I exaggerate, but I certainly didn’t do a lot of work.

This time, Gus said a few magic words that made it click. Ie. he said the opportunity was very similar to Leon’s. Partly because the opportunity at Leon’s is so great, and partly because I am more comfortable analyzing furniture stores, I decided to rectify my mistake not looking at BMTC in enough detail.

Lucky for me, BMTC has done nothing for well over 10 years, so I didn’t miss anything.

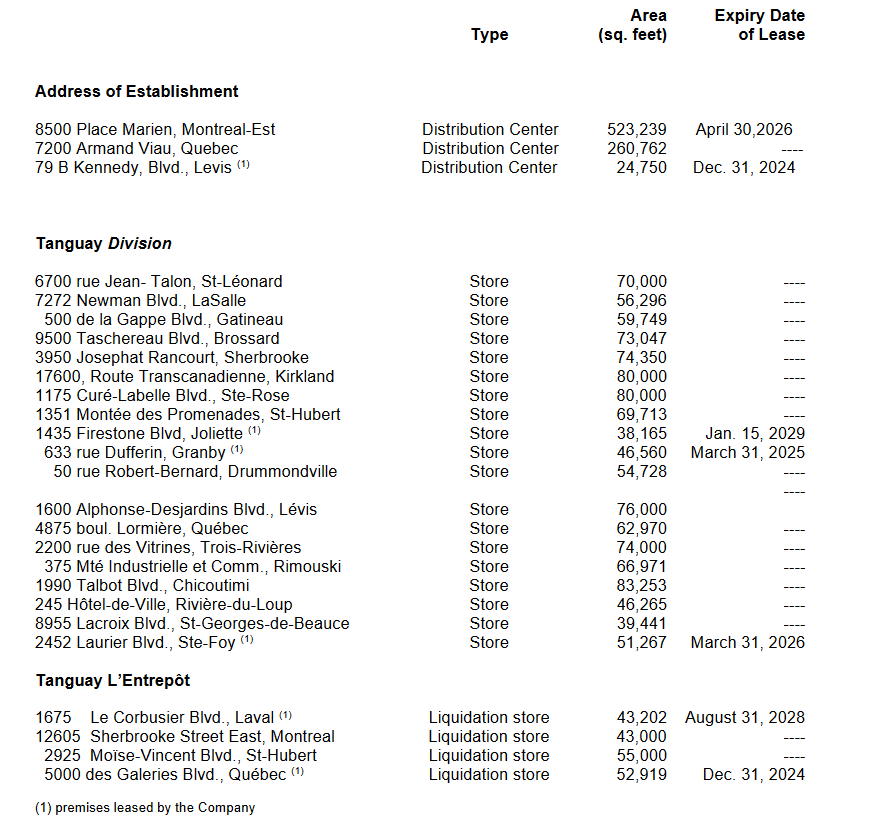

For those that don’t know, BMTC Group (GBT on the TSX) is a furniture retailer operating exclusively in Quebec. BMTC (which stands for Brault & Martineau, Tanguay, and Cantrex, the three companies which have come together to make up BMTC) operates 24 furniture stores in Quebec under the banners Tanguay (20 stores) and Tanguay L’Entrepôt (4 stores, a discount/liquidation chain).

I mentioned in my Leon’s post that Leon’s has a dominant position in Canada. Approximately 1 in 10 furniture stores in Canada is run by Leon’s, and Leon’s has 12-15% market share nation wide.

Quebec is a different animal though. It has barriers to entry with its burdensome language laws, and Quebecois tend to have protectionist attitudes. I am decidedly an Ontarian, but I’m pretty sure if you give any resident of Quebec the choice of buying a couch from an Ontario company like Leon’s (founded in Welland, ON) or a Quebec company like Tanguay, they are going to choose Tanguay all things being equal. I’m sure that many would pay more (how much more I have no idea).

While Quebec has about ~22% of Canada’s population, and its furniture market is around the same percentage of Canada’s furniture market, Leon’s has a little under 10% of its stores in the province (28/300). Assuming these stores are of average productivity (Leon’s as a whole averages ~$10 million in sales per location), Leon’s has just 5.2% market share in Quebec, much lower than its national market share (which actually suggests outside of Quebec Leon’s has even higher market share than I estimated).

Using similarly elementary logic, Ikea (3 stores in Quebec out of 16) likely has ~$600 million of its sales in Quebec, so a bit over 10% of the market.

BMTC on the other hand has 10% or more of the market. At one time it held over 30%. Without paying for data I only have old data or estimates of the size of the Quebec furniture market, but this source says the furniture market was $5.8 billion in 2021. That year, BMTC Group had revenues of over $800 million - note the fiscal year ends January 31st - suggesting market share was almost 14%. BMTC’s revenue is down considerably since, but it is likely that the Quebec furniture market is as well. BMTC had same store sales (SSS) decrease by 17% after dropping in 2022 as well. I don’t know for sure if BMTC gained or lost market share. Looking at Leon’s results from 2022 and 2023 (much smaller drops in revenue and SSS) would suggest that BMTC lost share, but this commentary from BMTC’s last annual report suggests Quebec may have seen an outsized decrease in its furniture market…

According to economists, the province of Quebec has been the most affected by this economy and will continue to underperform compared to the rest of Canada, due to the debt level of Quebec households and of the slow demographic growth of the province compared to the rest of Canada, which favorably stimulated the economy and helped support the labor market

The last observation, but not the least, the year 2023 saw a decline of around 20% in the profits of Quebec companies. This decline is partly explained by the drop in purchasing power due to the increase in household debt and the inflationary impact of essential goods, despite the increase in wages paid due to the labor shortage.

…and therefore it’s tougher to tell how market shares have changed. Regardless, exact numbers aren’t that important. The underlying point is BMTC has very high market share in Quebec, at least comparable to what Leon’s has nationwide, and BMTC is likely beating the nation’s leading furniture retailer in Quebec. Like Leon’s in the Canadian market, it seems BMTC and Ikea are in a class of their own in terms of market share.

In the fiscal year that ended January 31st 2024, BMTC lost $3.5 million, ~$0.10 per share. That’s not entirely indicative of the company’s earnings power though. During the year, BMTC changed all of its store brands to Tanguays, and as a result closed 5 stores. Operating five fewer stores hurt results, as did whatever closing costs were entailed there. Additionally, BMTC spent $15.5 million during the year to renovate the stores that changed brands and remained open. Another $4.5 million is being spent this year to complete the process.

So far in 2024, revenue is up slightly, and SSS is up 2.2%, so there are signs that the furniture market might improve going forward. This was a business that was earning $30-$40 million a year pre-COVID, while running a very inefficient organization with 3 store banners running independently with no integration at all. Revenue is a lot lower, and while BMTC’s retail operations will not earn $30 million this year, or next, it could get back there if the Quebec housing market/starts picks up, or the economy improves a bit.

But like Leon’s, the most interesting thing is not the furniture business.

Much like Leon’s, BMTC has been very conservatively managed. It owns the vast majority of its real estate…

…and BMTC has started to monetize this value.

Last year, it sold its Montreal distribution centre listed above in a sale-leaseback for $66.5 million ($255/sq.ft). There are now two development sites where BMTC has advanced plans to redevelop former stores, and the company is exploring the merits of redeveloping a third location.

BMTC has not talked about spinning off a REIT… it would be silly. But that doesn’t mean the real estate doesn’t have value.

BMTC’s real estate would not be worth $200 per sq.ft as Leon’s probably is. A lot of the square footage is a distribution centre in Quebec City, where recent transactions suggest the fair value is around $100/sq.ft. Additionally, while retail real estate in Montreal has been selling for $300/sq.ft, BMTC stores would not be on the higher end of values, and retail in Quebec City, Rimouski, Saint-Georges, and Saguenay definitely isn’t selling for $300/sq.ft.

Nobody is coming out and buying all of BMTC’s real estate, but if management made the effort to sell all of it piecemeal I think it could probably get $130/sq.ft. That would value the 1.4 million square feet at $180 million.

Importantly, BMTC would probably have to pay between $14 million and $20 million to rent the real estate it currently owns, and after ridding itself of property expenses, its earnings might drop $10-$15 million.

In addition to the real estate, there are two development sites in Montreal to consider. The first:

The Company entered into a partnership agreement with Urbania, who will be responsible for the development and construction of its property at 500 boulevard Le Corbusier in Laval into several residential rental towers. The Company intends to finance this real estate project at 75% with a long-term mortgage. The estimated value of the entire project is approximately $600,000,000. The Company created a new subsidiary, Le Corbusier-Concorde S.E.C. for this real estate project on January 31st, 2022. This real estate project should begin in the summer of 2025 as we are still waiting on approval of all permits with the city of Laval before we begin the construction phase. Once construction begins, the project should span over a period of 8 to 10 years with the construction of 5 rental residential towers for a total of approximately 1,200 doors.

This project is farther along, in the sense that it has a subsidiary created for it, BMTC has a partner to develop it, and while it’s unclear where in the process permitting is, the company would not be saying construction “should begin” in 2025 if it wasn’t very close to being fully permitted.

I’m skeptical about the $600 million value BMTC quotes. Assuming there is nothing but the 1200 apartment units, that would be $500,000 per door. While that isn’t unheard of, it is a very high valuation. InterRent and Crestpoint recently announced they had acquired a brand new building in very downtown Montreal for ~$430,000 per door. Sure this development won’t be ready for 10 years, so maybe $500,000 per unit will make sense at that point, but it certainly isn’t a conservative valuation.

Regardless, the project isn’t worth $600 million now. What might it be worth? A value of $50/sq.ft, which seems like a fine estimate for a project so near to breaking ground, value the project somewhere around $100 million. Applying a price per acre from comparable transactions yields a similar value.

The market has known about this development since at least June 2021, but between the timeline getting pushed out and it being a long timeline to begin with, the ambiguous wording/disclosure, and the uncertain value, I don’t think the market is appreciating this value.

Now the company has recently announced that it plans to develop on the site of another closed store.

The Company intends to proceed with the real estate development of several rental residential towers on its property located at 125 boul. Desjardins Est in Sainte-Thérèse. This real estate project is currently in the exploratory phase and the Company has identified a potential developer for the project. We should be able to announce during this financial year the details of this real estate project.

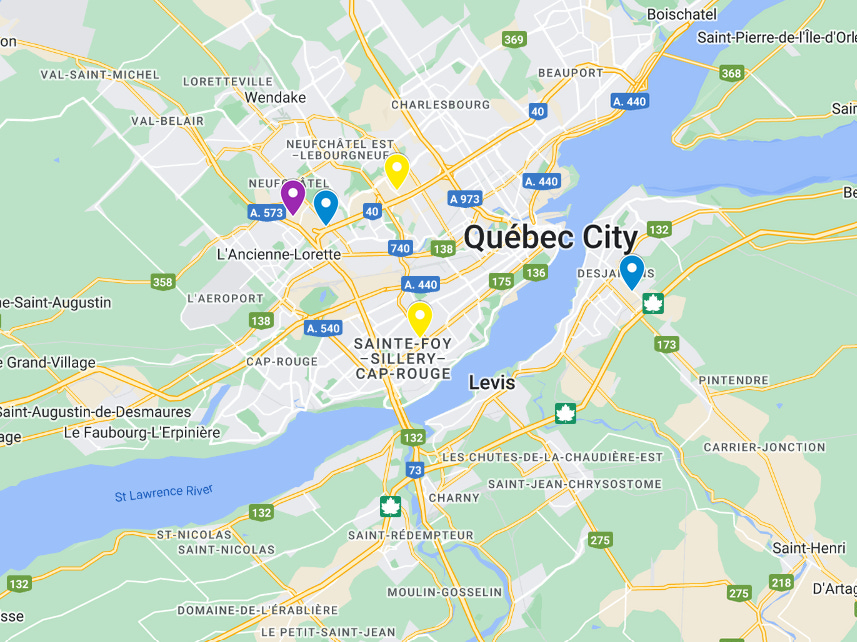

This site is even farther out from Montreal than the Laval project (it is the outermost red tag in the Montreal map above), but it is 6.5 acres that are worth something, and that 6.5 acres isn’t currently earning any income. Any value at all that can be realized is a positive.

I won’t attempt to put a value on this. There are too many possible outcomes, including nothing happening at all, so it would be a fool’s errand.

There are two more lines on the balance sheet that I need to talk about.

BMTC has almost $200 million of “other financial assets”. What are those exactly?

That’s over $1 per share of cash and almost $5 per share in investments. For years the company has been investing its spare cash in bonds and equities. It’s a little strange, but I do get the appeal of a large cash balance to a somewhat cyclical company, and I also understand wanting to earn a return on that cash. There isn’t disclosure about what the equities are, but from what I can gather it seems like the money is conservatively invested - I’d guess BMTC is more likely to own Microsoft than Microstrategy.

As a shareholder I’d probably prefer the money be used to acquire more market share by buying out competitors, or buyback shares, or pay a special dividend. But as far as wrinkles go, a company having a lot of cash and investments isn’t a bad one.

And actually, we can’t fault the company too much about how it is returning cash to shareholders. Since 2018, the dividend has increased 50% from $0.24 a year to $0.36 and since the start of 2018, shares outstanding have gone down from 35.1 million to 32.4 million today. There are many companies that have done less.

Still, you wonder what edge the management of BMTC has in investing in public equities? Let’s give management the benefit of the doubt and say they really know the furniture business. BMTC is family owned and has been for a long time. I’m comfortable making that leap. But are the managers good investors? What proof is there of that?

Along the same line, are they good real estate investors?

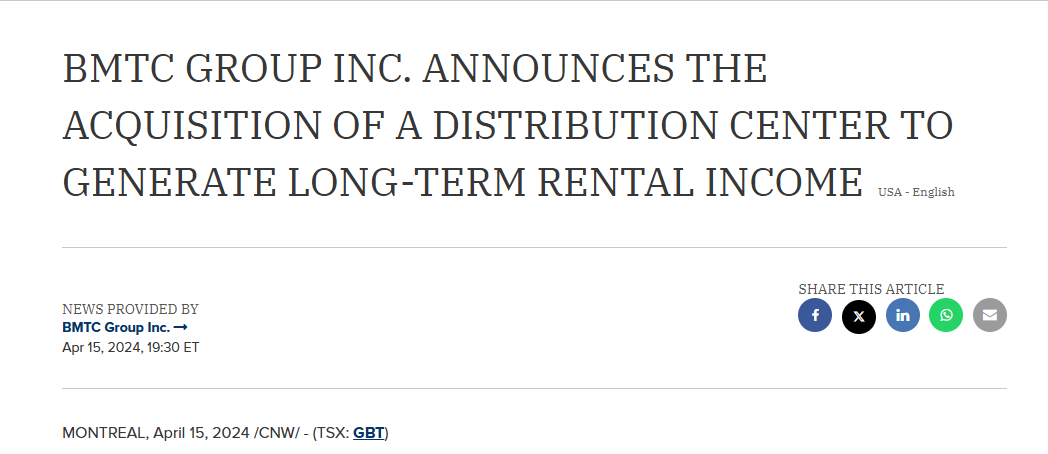

This year, after selling its own distribution centre a year before, BMTC bought a RONA distribution centre for $96 million with the intent of being a landlord to others.

The development projects on its own land are one thing. If you have excess land, developing it is one way to extract value from it. Maybe you’d be better off selling it to a developer than getting into the development business yourself, but whatever. You own it and you want your money’s worth. Fine.

But getting into the landlord business… forking over cash that belongs to shareholders (to be fair, management owns almost 70% of the stock so it is very much their money) to diversify into a business you’re only tangentially familiar with… that’s another thing. Sure, Yves Des Groseillers (founder and chairman of the board) bought the locations of his stores, so he knows a bit about real estate. But I’d argue that’s quite different.

I do not know if this was a good purchase or not. It might have been. All I know about it is that it was built in 2006 and is ~380,000 sq.ft. At recent sales prices of ~$200/sq.ft in the Montreal area, the purchase does not seem like a bargain, but I’ll also note that there is nothing saying the value couldn’t be higher than those recent prices.

Interestingly, BMTC is currently holding this property with no mortgage on it, whereas management has already said it would have a 75% LTV mortgage on its Laval development, even though it’s not going to be complete for 10 years. I’m assuming that management doesn’t see the need to mortgage the property when the company is also sitting on $200 million of cash and investments. At some point though, this property could be prudently mortgaged and BMTC could pull $50 million out of it or more to fund Laval’s development, or buybacks, or dividends.

Let’s add this up like we did for Leon’s.

The Laval development is worth $100 million, or ~$3.00 per share.

The real estate is worth $180 million, $5.50 a share.

The cash and investments are worth ~$6.00 per share.

I know the income property was just purchased for $96 million this year, but let’s say it’s worth $75 million, which is roughly the $200/sq.ft average price of industrial real estate. That’s $2.30 per share.

Adding those up we’re at almost $17.

I have not included land in Levis that BMTC just bought this year for $22 million (the site of a future distribution centre). I haven’t included an $86 million surplus in its defined benefit pension plan. And I haven’t gotten to its furniture business.

The value of the furniture business (which BMTC now refers to as its Tanguay division) is the hardest to determine. Revenue is much lower now than it was pre-Covid. In 2016, BMTC had $746 million of revenue.

2018 revenue was $742 million.

2019 revenue was $720 million.

After overearning in 2021, 2022 revenue was $718 million.

2023 revenue was down all the way to $578 million, and 2024 doesn’t look like it will be much better.

I don’t think that the dropping revenue is a death knell, nor an indication that the business is bad. But BMTC needs to show better results from the Tanguay division. There are signs of that. While sales aren’t growing the way you’d want them to, the bleeding does seem to have stopped/slowed and revenue is flat year over year.

In 2023, administrative costs decreased by $22 million, but more tellingly dropped as a percentage of revenue from 7% to 5%, presumably as a result of changing all stores to Tanguay banners and integrating back office functions more. Administrative costs have dropped to 4.6% of revenue through the first half of 2024. BMTC also managed to cut $10 million of operating expenses in the first half, including $6 million in the second quarter. The company definitely seems to be running leaner, which was low hanging fruit for boosting earnings.

The Montreal distribution centre seems to have been less than ideal for Tanguay’s needs, hence selling it, so the new Levis distribution centre (likely 2-3 years away from being ready) likely will cut some costs as well.

Presumably, after spending the money to change all these stores to Tanguays, BMTC is no longer going to be closing stores, so that headwind to sales should go away.

I don’t know if I’d call Tanguay a turnaround, but there are improvements that can be made, and to management’s credit look like they are being made. It makes it very tough to apply a multiple to what the business might be worth when the earnings are so up in the air. And shortly, unless BMTC improves its disclosure, the real estate division will mask the results of Tanguay. Both the income from the income property (and any others that are acquired in the future) and the expenses of the developments will make it very tough to tell what Tanguay is earning. The stock barely moves (see stock chart above) but with any other stock the skewed earnings might create irrational price movement.

As it is, BMTC is trading for roughly 0.75x sales. That’s a terrible metric I know, but revenue is about the only number I can be comfortable with. Leon’s, a superior business, trades for ~0.55x sales. But both of these companies have a lot of value outside of the furniture business.

I estimated that after accounting for its real estate and land value, approximately $400 million of value was attributed to the Leon’s operating business. In that case, the sales multiple is just 0.24x.

I argued that Leon’s was worth much more than the stock price implied, hence the fair value of the business was higher than 0.24x, but we can imagine a world where the stock price of Leon’s is right.

If the fair enterprise value of Leon’s’ furniture business was 0.24x sales, what might the fair value/sales multiple of Tanguay be? 0.12x? That would be $2.10 per share.

We can also look at two relatively applicable acquisitions.

Sleep Country was acquired by Fairfax for ~1.7x P/S. Again, Sleep Country is a much better business than Tanguay. I know it’s not the most comparable.

When Leon’s acquired The Brick, way back in 2012, it paid a little more than 0.5x sales. Despite the deal being 12 years ago, it does have some applicability to today. The Brick was an underperforming competitor, and was a strategic acquisition made by a smart acquirer. The Brick is a much bigger bigger company than Tanguay. The brand is better recognized. It would have created more synergies, etc. It would be worth more to an acquirer.

But BMTC/Tanguay is not without its value. As I mentioned, Tanguay probably has 10-15% market share in Quebec. It offers a way of breaking into the tricky Quebec market that not a lot of other retailers probably do. And given its small size and the cost cutting the company has already shown, it seems very likely that a large acquirer could squeeze a lot of synergies out of Tanguay (including an almost $2 million management fee that BMTC pays to the Tanguay family for managing the division).

For these reasons, Tanguay could be seen as a similarly strategic acquisition. I don’t think it’s out of the realm of possibility that it could fetch 0.5x sales in an acquisition. That would mean around $9 per share.

And finally, we can apply a modest multiple to a very rough estimate of what earnings might be post cost cutting/integration while imagining BMTC is paying rent on its stores. I can see this business earning ~$10 million in such a scenario. I don’t think this estimate relies on rosy glasses. It probably takes some operational improvements and some sales growth and/or a better consumer environment, but it is not an irrationally high estimate.

We can see that with roughly equal revenues to now, in 2000 the company was able to earn $21 million, in a different but still not great time to be a consumer.

It’s also interesting to see that not only has revenue been dropping in the last few years, revenue has not changed (in fact is down slightly) going all the way back to 2000! 24 years!

If we add up the value of what BMTC owns, we get a sum of the parts of $20-$25. Not bad for a $13 stock. That would seem like a no brainer.

But there are question marks and wrinkles.

The value of Tanguay, and whether it can improve its results and start showing profits, is one of the biggest questions. But when looked at as a proportion of the value, it really isn’t. If we write off Tanguay to zero, we can still say BMTC is worth $17 or more.

The question marks around the rest of the value are much more important to the prospective investor.

All of that $17/$550 million of value is entrusted with management to allocate accordingly.

The Rona distribution centre is purchased, no going back on that now, but this language is in the latest MD&A:

The Company is currently evaluating renovation costs in order to make the distribution center more efficient by automating in order to create greater lease value.

And that same sentiment has been mentioned several times. It is possible that management makes a poor decision to invest more money into this property and doesn’t realize a good return on it.

The development in Laval is a huge question mark. BMTC has an experienced partner, but management would hardly be the first people to lose money by getting into the development business. To be taken by an experienced developer. To have a construction project go over budget and/or finish behind schedule. While the land might be able to be sold to a developer for $100 million now, and the project might be worth $500 million in 10 years or so once it’s completed, if the project is mishandled it could be a money pit. It could be worth a lot less than $100 million. It could be worth nothing. The company could end up spending millions and the project never be completed, hence end up being worth a significantly negative value.

The owned real estate should be a relatively stable asset, but it does need to be kept up.

Finally, there is $200 million of cash and investments. This is only worth $6 a share if the company gives it to shareholders, through either a dividend or buybacks, or if the money is invested well. As it is, it looks safe to assume this money is earmarked for real estate.

In an interview, CEO Marie-Berthe Des Groseillers (daughter of the founder Yves) announced the company would be building two new distribution centres totaling 600,000 square feet. That will end up costing $50 million or more.

Building 1200 apartments on the Laval land, even financing it at 75% LTV, will probably take most of that $200 million on its own. If the Ste-Therese development goes forward, there goes another $100 million or whatever. And it seems inexplicable for management to purchase that Rona distribution centre, if they didn’t desire owning more properties.

You need to have faith that management is going to allocate the capital well. More so than with many companies, BMTC’s value depends entirely on capital allocation.

Because of the question marks around what management will do with its capital, I think the best case scenario for shareholders is for BMTC to be acquired and/or taken private.

That range of $20-$25 I believe is a good starting point for what the stock would be worth to an acquirer.

Leon’s is the natural acquirer to consider. It has the financial capacity - little debt and a net cash balance sheet and an inflow of cash coming from its REIT IPO - and it has shown a willingness to grow by acquisition before. In fact, acquiring BMTC would cost roughly as much as it cost to acquire The Brick in the early 2010’s.

If Leon’s saw the Quebec market as one it wanted to expand in, there would be no better way to grow there than to buy all of BMTC, or just Tanguay. Acquiring the whole company makes sense given Leon’s has an easy way to monetize the real estate. Packaging up BMTC’s real estate into the REIT would make the REIT bigger, more liquid (assuming it would issue units to acquire the real estate or would be more in demand if done prior to the IPO), and more diversified geographically. Buying BMTC and then selling the real estate and developments to the REIT (which presumably will be able to issue units to finance such a purchase) would mean Leon’s itself would be paying remarkably little to buy a lot of market share in Quebec, even at a large premium to today’s price.

I don’t think there’s any question Leon’s would be interested in buying it. There are two big question marks though:

Would the Competition Bureau and/or Province of Quebec allow the deal?

Would the Des Groseillers family sell?

I don’t know the answer to number 1, but I could see it being a problem. The protectionist attitude of Quebec cuts both ways. I could see the province raising a stink about one of its old homegrown companies being sold to a large Ontario competitor. I could also see the combined market share of a Leon’s/BMTC merged company being judged too much in the province. While its share wouldn’t be that high, we have seen overly aggressive enforcement of these issues in recent years. It seems like every deal gets scrutinized. Even though I’m pretty sure the combined market share would be less than 20% in Quebec, it still seems like it would be a long drawn out acquisition.

As for number 2, I don’t know that either but I suspect the family would not be interested in selling.

While Yves Des Groseillers is getting up there in years, his daughter is now running the company and she is in her mid-40’s. She has a long career ahead of her, and in her brief press interviews she discusses long term strategy. If she is starting major developments that are expected to take ten years to complete, it doesn’t seem like she is looking to give up her job. I suspect she wants to reap what she is sowing.

The Des Groseillers family owns over 63% of the company, so it needs to be on board with any sale process. That said, it’s at least possible the family would be interested in selling the furniture business in order to focus on its real estate operations and managing its investments.

The other thing that could happen to surface value quickly is the Des Groseillers family could offer to take the company private. Yves has already tried this once, offering $16.50 to take the company private in 2009.

That offer failed, but at the time BMTC was a fast growing, well run company. Now BMTC has only briefly traded over $16.50 twice in the last ten years. Other than the family, Fidelity is the only shareholders of any consequence. Fidelity owns a little under 4.1 million shares, 37% of the shares not owned by the Des Groseillers. Fidelity’s support would be important to any privatization.

I’m taking a guess that most minority investors would happily accept $18 for their shares, given that’s about as high as they’ve traded in the last ten years, I expect many will have anchored to that price. Fidelity should be happy to accept that too seeing how long it has had money tied up in BMTC and how little the stock actually matters to it - Fidelity has trillions in AUM, and BMTC is just a 0.2% position in the fund that owns most of the stock (Fidelity Low Priced Stock Fund). That said, maybe Fidelity anchors to a higher price, or holds out for more, or whatever.

For the Des Groseillers family to take the company private at $20 would cost them $220 million. That’s not insignificant by any means, but the company can easily come up with the money, between the cash and investments owned by the company and the capacity to borrow against the real estate, it’s likely that the Des Groseillers could buy complete control without a penny out of pocket. I’m pretty sure that they could buy the company with no money out of pocket and then pay themselves a big dividend for their trouble.

Unfortunately, that high ownership cuts both ways… there is no way for anyone to push for change at BMTC. Nobody can acquire a large position, given the low liquidity, and if they did there’s no way to sway management given management own far more than anyone else ever could.

And with that I think I’ve come to the end.

I don’t really have a good conclusion on whether BMTC Group will be a good investment. I don’t know whether I’ll buy it.

On the one hand the value of the assets, without considering its operating business, easily add up to $17, compared to the current $13 stock price (a price it has hung around for years). The furniture retailing business looks bad superficially, but I think there’s enough good that it could be turned around. The change to all stores being branded Tanguay and finally integrating its stores is new, but we’ve seen positive signs in terms of cost reductions and revenue has at least stopped falling for now. And even if the business couldn’t be turned around, there is a well capitalized acquirer which on paper makes a lot of sense to acquire BMTC or Tanguay. It’s also always possible the Des Groseillers tire of the public markets and take out minority shareholders. If either Tanguay’s results improve, or BMTC’s new real estate ventures go well, or BMTC/Tanguay is acquired or taken private, the stock should be a home run.

On the other hand, any acquisition of BMTC or Tanguay by Leon’s in particular is likely to face regulatory pushback, which probably wouldn’t kill a deal but does make an offer less likely. And if no offer comes, we’re left with a furniture business which has seen revenues and store count shrink for years now, with an entrenched management team that has overseen that decline still running it. Not only is that management team the one in charge of turning around the retail business it has shrunk, it is now also diversifying into income properties and real estate development. If management can’t turn around its furniture business, and isn’t adept at real estate, that $6 per share of cash and investments will earn poor returns and probably never make it to shareholders. The furniture business’ value would start on the lower end of the ranges I stated above and only go down. The real estate it owns will probably not be monetized well and if it is the proceeds will just be reinvested into different real estate which we can’t really trust them to acquire or manage well.

The value is there, but I don’t know if I have enough faith in management to steer the ship.

Interesting find, thanks for sharing.

I’ve been intrigued by BMTC since pre pandemic.

I think the company’s strategy is simply to harvest cash-flows (and real estate) from the furniture business and continue to plow it into a real estate empire. It’s probably quite tax efficient for the family to keep all the money in the mothership and find things to invest in, instead of paying it all out to shareholders.

Going forward, I think this will end up being this large semi-private real estate holdco for the family. Gives them lots to do and opportunities for jobs for more of the family members.

Might end up being a decent investment so long as they don’t overpay for their real estate investments. Given the discount to NAV, a little bit of overpaying won’t kill the thesis.