Pollard Banknote

As I was finishing up this piece, Pollard reported terrible first quarter results, which even the company had to be blunt about. “The first quarter was a very challenging quarter generating poor financial results,” stated John Pollard, Co-Chief Executive Officer.

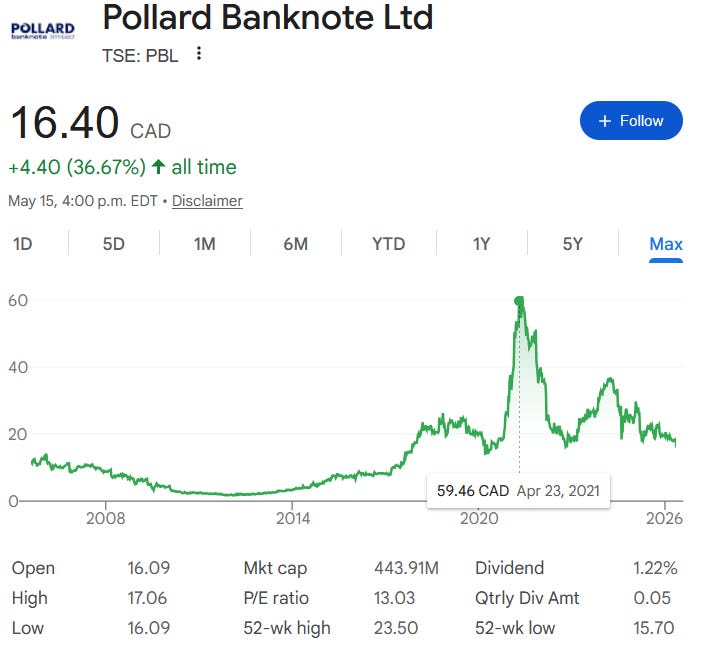

The poor results are described as being due to temporary factors, or are a result of timing of sales, and the press release gives reasons that the rest of the year shouldn’t be too far off previous expectations. The results caused another considerable sell off. When I started my research, Pollard was around $18. It’s now down to $16.40.

What I found interesting in the press release was the announcement that Pollard intends to initiate a share buyback. As far as I can tell, Pollard hasn’t ever bought back shares, or definitely not in any size. A share buyback now tells me that management sees what I’m seeing. Presumably management has concluded that there will still be some capital to buy back shares after investing in its own businesses and after any M&A that is prudent. When a family that owns 64% of an illiquid stock announces their first ever buyback, it’s definitely worth noting.

Pollard Banknote has an interesting stock chart.

Looking at this, you’d think it was some unprofitable software company, or became a meme stock, or was a general shitco that got bid to the moon in 2021 like every other shitco did.

Pollard is a manufacturer of instant lottery tickets, and produces supplies for the charitable gaming market. It’s involved with Bingo, not Bitcoin. So why does the chart look like that?

Well Pollard also provides iLottery services, or lottery on the internet. As you may remember, back then people were locked in their houses, and the government was giving them free money. If you’re home with money you don’t need, what else are you going to do besides blow the money on the lottery? And if you’re locked in your house, the lottery on the internet is the only game available.

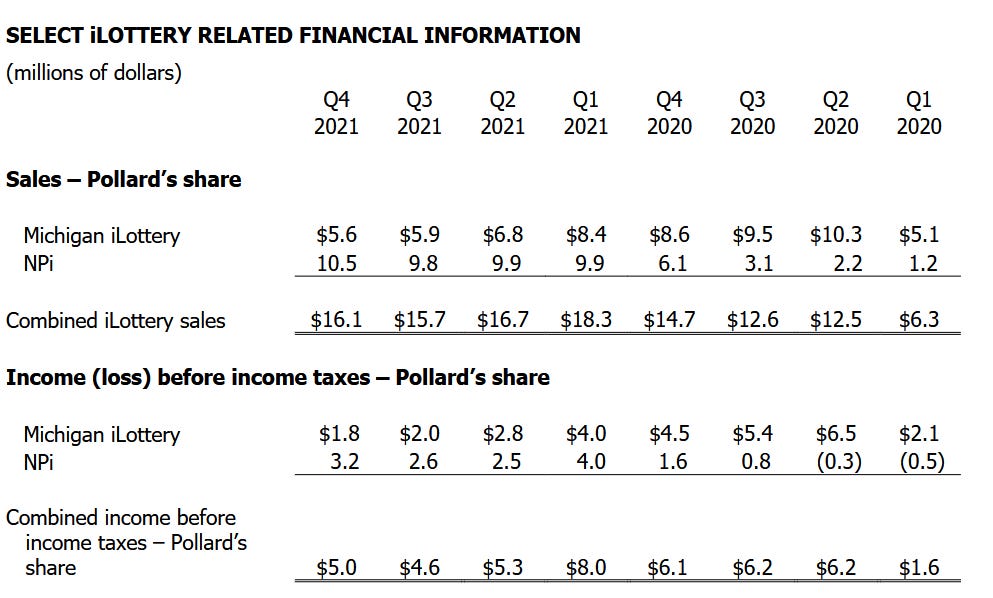

Pollard provided its iLottery business through two joint ventures. One was called “Michigan iLottery”. This was a 50-50 JV with NeoGames. It won the Michigan contract in 2013 and the iLottery program went live in 2014.

The other JV was also 50-50 with NeoGames. This JV, called NeoPollard (NPI), came after the Michigan deal and formalized the relationship a little more. Pollard in its iLottery results would report both lines, but the point was Pollard owned 50% of both JVs with the same partner.

It was a good relationship.

The bulk of the thesis with Pollard in those crazy days of 2020 and 2021 was that iLottery was going crazy, and NeoPollard was going to be the largest player in the industry.

I looked at Pollard sometime during its run up. I ended up not buying any, nor really finishing my research, though at this point I can’t say why.

Connor Haley of Alta Fox Capital wrote a very thorough report on Pollard around the same time, and I’d highly recommend it even if it’s five years old at this point. One, because it is very well done. And two, because it offers a glimpse of what the market was thinking at the time.

Alta Fox Capital - Pollard Banknote

So what caused the violent crash after the run up?

Well, part of it is Pollard suffering the same fate as all the other shitco stocks. The run up was too exuberant, so the crash was violent.

What hurt a lot of the shitcos was inflation (and by extension, interest rates). Inflation hits Pollard hard.

A substantial portion of Pollard Banknote instant ticket business is based on long-term fixed price contracts with its lottery customers and therefore cannot adjust its fixed contractual product pricing. As a result if Pollard Banknote were to experience sudden and significant inflationary cost increases on our manufacturing inputs including raw materials, could have a significant negative impact on Pollard Banknote’s business, financial condition, liquidity and results of operations.

Source: Pollard Banknote 2025 Annual Information Form

Our instant ticket customer contracts are primarily long term with fixed pricing. As such, in the short term we were unable to pass on these significant cost increases and our instant ticket margins underwent a very negative reduction.

Source: John Pollard, Pollard Banknote 2023 Annual Results Press Release

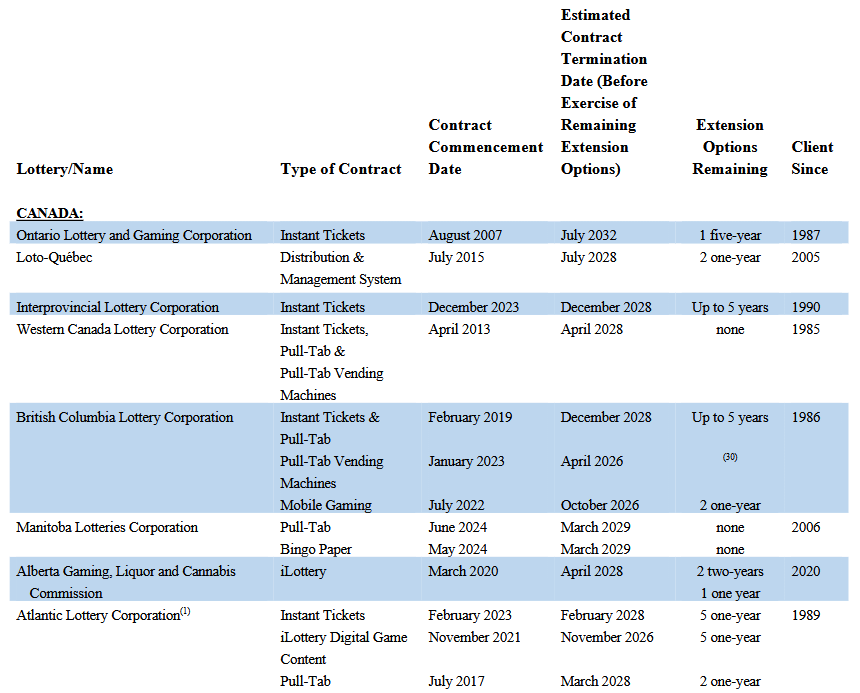

Pollard signs long term contracts with its instant ticket lottery partners, typically 5-6 year contracts but sometimes considerably longer, without the ability to raise prices. The printing business is essentially short inflation.

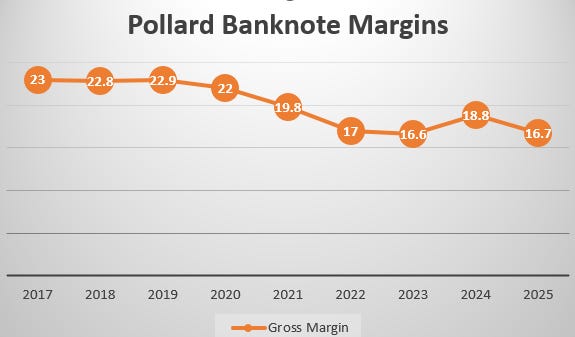

We can see the effect inflation has had on Pollard’s gross margins.

Margins had been pretty steady, and now Pollard is keeping 4 to 6 cents fewer of every dollar than it was pre-COVID.

There was one other big contributor to Pollard stock’s crash, but it was more of a series of events that all culminated in a big hit to the business.

NPI was racking up iLottery contract wins, exactly as predicted. It had the iLottery contracts for Michigan (not really NPI but you get it), New Hampshire, North Carolina, and Alberta. NPI was the premiere iLottery partner. From what I can tell it won half of the iLottery contracts given out during the time period starting with the Michigan announcement and ending with NPI winning the West Virginia contract in 2024, the most of its competitors. It was clearly a huge winner for Pollard Banknote. The iLottery thesis was playing out exactly as bulls had hoped.

In January 2023, Pollard “formalized” its operating agreement with NeoGames regarding NeoPollard.

It was described as "[reinforcing] the long‐term approach to ensure the continued success of NPI and accordingly, the operations of its market leading customers.”

That’s all fine and good, but I don’t know what it means. The next line in the press release is very clear though:

In addition, the Agreements allow Pollard and NeoGames the option to pursue future iLottery opportunities in the North American market either in partnership, as part of the Joint Venture, or independently.

Looking at the chart, the market didn’t really care about this announcement. Maybe it was seen as bad news, but the stock was low enough already. I don’t know. There was not the drop there should have been in hindsight.

Then in May that year it was announced that NeoGames was being acquired by Aristocrat Leisure, for $1.2 billion USD. The market still didn’t care.

In October 2023, NPI won the iLottery contract in West Virginia. The market clearly liked this, and Pollard stock had been going up throughout 2023, but this announcement gave it a pop and it continued to rise thereafter.

The stock peaked in April 2024 around $36.

Then in June it was announced that Aristocrat alone would take on the New Hampshire iLottery business, which had previously been NIP’s contract. The new owner of NeoGames had bid on NPI business on its own, and won. Pollard stock got hit hard on the news.

Two months later on August 6, it was announced that NPI’s Michigan iLottery contract wouldn’t renew in July 2026 when it expires. Again, Aristocrat was taking the business.

Pollard stock tanked 30% on the day, as it should have.

Pollard was a 50% owner of a JV which was the market leader in iLottery operations. It probably would continue winning 50+% of all iLottery contracts given out. And iLottery was a huge grower, between more jurisdictions starting operations and existing operations growing organically. Unfortunately, Pollard’s partner was the technology behind the business, so it was arguably the more important partner. The alpha partner had decided it could do things without Pollard, and now it looked like all those iLottery earnings were going to disappear. Aristocrat could approach the lottery commissions as NPI’s contracts neared expiry, and win the business for itself, keeping 100% of the profits instead of sending 50% to Pollard. Its partner was now a cut throat competitor.

New Hampshire was described as not material after the contract expired, but Pollard’s share of Michigan iLottery earnings was $9 million EBITDA, ~7% of Pollard’s total EBITDA.

One final note on what affected Pollard’s stock during that free fall. Michigan iLottery sales had been growing a lot, but that slowed then stopped during the last few years. In fact, sales were lower in 2025 than they were in 2024. Given that Pollard is losing this business, that isn’t a huge tragedy, but it could be and probably was seen as a bad sign for other iLotteries. Perhaps the sky is not the limit.

When valuing Pollard I think a sum of the parts analysis is illustrative, because the legacy businesses of ticket printing and charity gaming are so different than iLottery. And while one of those parts might generate a lot of cash now, it’s probably coming to an end so valuing it separately makes the most sense to me.

Charity

In 2025, the charity business had $156 million in sales. Gross margins were impacted by Minnesota, which has the US’s highest charitable gaming revenues, changing its laws around electronic pull tab games (some features were deemed too close to slot machines which only Native Americans have the right to operate in the state). Pollard had to change their games, less games were played, etc. Even so, by the end of the year, gross margins were approaching historical levels. Let’s call gross margins 22% going forward for sake of argument.

Charitable gaming revenues grew ~13% in 2025, which was mostly the results of two bingo acquisitions, Pacific Gaming and Clarence J. Venne. I wouldn’t expect much organic growth in this business, but it’s a fragmented market with a variety of products, and I expect that Pollard will be able to continue making acquisitions like Pacific and Venne to grow.

In 2026 the charitable gaming business should have sales around ~$160 million and gross profits of ~$35 million at my assumed 22% margins.

In 2025, Pollard’s overhead (which I’m calling its administration and selling expense lines) was ~$100 million. That’s handy. It’s always hard to estimate how much overhead cost is associated with each of a company’s businesses. In this case, I’m guessing that ~$35 million is attributable to the iLottery business as Pollard invests heavily into it to get it to scale. The remaining $65 million is split 75%-25% between the printing and charity operations.

If I’m close in that estimate, Pollard’s charitable gaming operations are doing ~$20 million of EBITDA.

In 2025, Light & Wonder purchased Grover Gaming’s charitable gaming assets for ~7.7x EBITDA. The assets were mostly eTabs (electronic pull tabs), so these were higher margin, higher growth assets, but I think that 7.5x EBITDA is a fair idea for what an acquirer might pay for Pollard’s charity business, especially considering Pollard is growing in the eTab space.

Hence I’m going to value this part at $150 million.

Print/Manufacturing

Pollard’s bread and butter. Pollard is one of the largest manufacturer's in the world, with about a 22% market share of the instant ticket printing market both in North America and worldwide. That market share has been stable for the past ten years or more, but might be set to tick higher as Pollard recently won the contract to be the primary supplier for the California lottery, versus its previous status as a secondary supplier. The California lottery is the second largest seller of instant tickets in the US, so it’s a big deal (total contract value estimated to be around $375 million) and it may serve as an indication of Pollard becoming more highly regarded.

I won’t go as far to say that Pollard is going to continue taking market share, or will win a higher proportion of contracts going forward, or anything. It’s not a bad sign though.

It’s one of just three manufacturers in the US, which is 57% of a growing global market for instant ticket sales.

It’s a high quality business, with long term contracts and relationships, and barriers to entry (it’s unlikely a new entrant will be trusted with such an important source of government funding, and there are legal barriers to entry in the US). Few companies can boast of such an enviable position.

In 2021, Alta Fox claimed 15x EBITDA as a fair multiple to put on this business for the reasons I stated above. That has proven to be optimistic in hindsight, and was probably a consequence of the exuberant market at the time. We have a few data points that 15x is too high.

In late 2021, after the Alta Fox report, Scientific Games sold its lottery business to Brookfield Business Partners for 12-13x EBITDA. Scientific Games is the giant in the industry, with ~69% market share.

The third competitor, much smaller than Pollard at ~10% market share, is Brightstar Lottery, formerly known as IGT. It’s public, and is trading at like 6-7x EBITDA.

I don’t think we can compare Pollard now to the Scientific Games deal in 2021. Just look at how much lower Pollard’s stock is now - it’s clear that these earnings are not as valued as they once were. At the same time though, Pollard’s instant ticket business is better than Brightstar’s.

I know it’s quite a spread, but I think 8-10x EBITDA is around fair for this business. I can’t give you false certainty or precision. It is a good business, and Pollard is a good operator, so 10x EBITDA isn’t unreasonable. At the same time, I want to be conservative and I have to acknowledge what the market is saying about Pollard and Brightstar.

Margins have recovered since the inflation troubles Pollard had, but likely are still going to be below what they were historically for a while. I’m going to estimate they’re ~20%. If that assumption and my overhead attribution are approximately correct, the “traditional” lottery/printing business is doing EBITDA of ~$40 million.

That makes this part worth something like $320 million to $400 million.

NeoPollard

NPI is a cash cow. Pollard’s share of the pre-tax income from the two iLottery JVs, Michigan and NPI, was ~$71 million in 2025 and ~$59 million in 2024.

The Michigan JV ends in June, but Pollard should harvest ~$4 million from it before then. I’m also going to make a pessimistic assumption, that I think the market is making as well, that as each NPI contract ends, Aristocrat will choose to bid on the contract on its own. In other words, the NPI JV is in runoff.

The JV has four iLottery contracts left. Three of those, Alberta, Virginia, and North Carolina, are set to expire at various points in 2028 (though the Alberta market opens to private operators in July of this year, so NPI will lose some of its monopoly status). That’s the big cliff. The West Virginia contract will last until 2033.

It isn’t all doom and gloom. North Carolina just renewed its contract in August 2025, buying NPI three more years. Virginia renewed its contract in January 2025. And all of the NPI iLotteries have options to extend them, so while I think it’s most likely that NPI loses each of these (if not in 2028 then after an extension or two), there is a chance NPI remains in business.

The JV likely has little to no terminal value; any value in it is the result of the contracts. No contracts, no value. But with a conservative estimate of the net present value of the cash flows Pollard will receive from NPI, I estimate NPI is worth ~$120 million to Pollard today.

If any of these contracts get extended, particularly North Carolina, the value increases of course.

iLottery

It probably sounded like I was bemoaning Aristocrat up there for killing off a golden goose, but one could say that it was Pollard that started the breakup of NPI.

In 2021 it acquired Next Generation Lotteries, which provided iLottery technologies.

The strategy really came together in August 2024 when Pollard won its first solo iLottery in Kansas.

Then just ten months later, Pollard was able to launch that iLottery, faster than any other implementation in the US to that point. The iLottery also set several records for usage and revenue as it started up.

Right now the Kansas iLottery is unprofitable for Pollard, but as it grows it is rapidly approaching profitability. The state has budgeted $71 million in iLottery sales for 2026. Are states good prognosticators of their budgets? No idea, but that is ~3x as much as was budgeted for 2025, and would mean ~$3 million of revenue for Pollard.

In October 2025, Pollard won the contract to be provide Belgium’s “omnichannel gaming platform.” This isn’t just an iLottery. Pollard has essentially been handed the keys to drive all of Belgium’s lottery operations.

The press release states the contract is worth ~$289 million over its twelve year term, so it's material vs Pollard’s $600 million of revenue in 2025.

Pollard also has a deal for eInstant games in Norway, Czechia, and Lithuania, as well as a digital player loyalty program for Oklahoma.

It’s not much if you compare it to Aristocrat/NeoGames, but it isn’t nothing, and there are enough green shoots to think this can be a very valuable business.

iLottery earnings are not split out in the financials, and with the revenues that are “digital” but not iLottery, like the Oklahoma player loyalty program, it would be tough to do. But I expect that in 2026 the online businesses will do something like $35 million, counting all of the Belgium contracts sales (which includes lots of non-tech sales).

Margins probably aren’t at the 50+% they should end up being, so let’s say gross profits are ~$10 million or so and EBITDA is negative $20 million.

At 4x sales, the standalone digital business is worth ~$140 million or so. That seems reasonable for a highly regulated tech business, when Aristocrat leisure trades closer to 5x and it acquired NeoGames at around 5x as well (depending on how you treat the NPI sales).

I’ll also add in $20 million for mkodo, which Pollard acquired in 2020 for $13 million. mkodo is a “a leading provider of digital apps and user interfaces for the lottery and gaming industry worldwide”, and which developed the leading technology iLotteries use to ensure the location of their users.

Add those together and Pollard’s iLottery business is worth ~$160 million.

With $178 million of debt, Pollard’s sum of the parts is $20-$24, depending on how you treat the manufacturing business.

That isn’t a whole lot of upside vs today’s price of ~$17. It might not be so bad considering markets today, but it’s not the type of no-brainer opportunity I’m usually looking for.

But I think if I am wrong about Pollard, it’s because I am being conservative.

The charity gaming business is very solid, and the changes in Minnesota mean it is currently underearning. I accounted for that a little bit by saying margins were 22%, but I think the charity business could still improve beyond expectations.

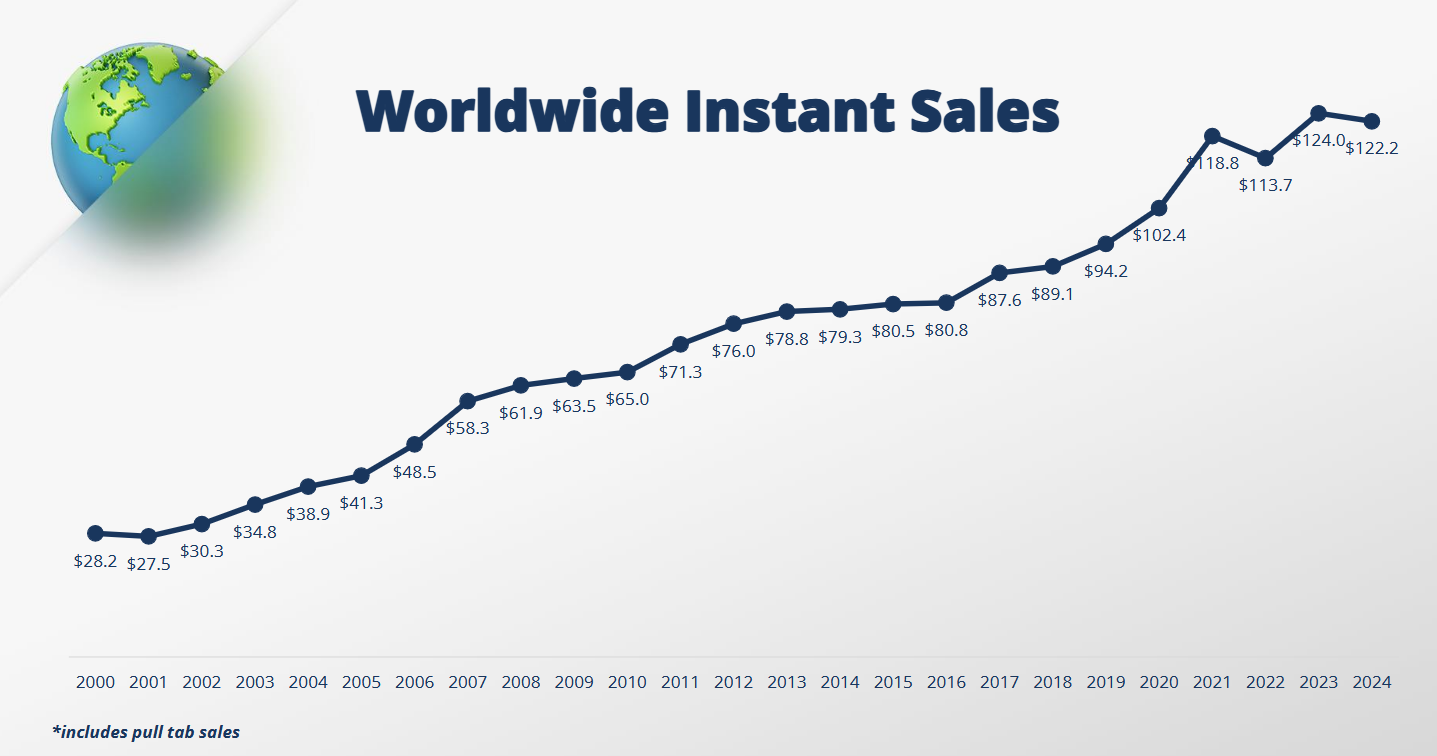

There is a chance that Pollard is able to take share in the instant tickets market, if the California win is a harbinger. And as can be seen in the graph above, that market has historically grown and has hit a bit of a plateau. If instant ticket sales pick up again, Pollard stands to benefit, and I think it’s valued as if the market isn’t going to grow. Maybe it won’t, or it will shrink, but I think pessimistic assumptions are priced in and a possible return to growth is being ignored.

At the risk of repeating myself, I assumed the most imminent possible demise of NeoPollard that can take place. There’s nothing to say that is a guarantee. Each of the lotteries has a say and can choose to renew with NPI. And why wouldn’t they? Their iLotteries have been very successful, and while the switch from NPI to Aristocrat is as low a risk as a switch can be (since the tech will be the same), there is still some risk. I would assume that Aristocrat pushes hard for North Carolina and Virginia, given their respective sizes, but West Virginia and Alberta are not unicorn contracts that are worth fighting tooth and nail over. And at least for Alberta, Pollard probably has a leg up on Aristocrat given the recent “Buy Canadian” attitude everyone is taking up here.

And Pollard’s iLottery business has a chance to be very big, if not NeoGames/Aristocrat big. Kansas is an indisputable success, and I think a lot of other similar states will probably look to that success and quick start up and it will weigh heavily in their own decisions.

The Belgium contract can also be illustrative here. Given Pollard is somewhat uniquely qualified to be the “omnichannel provider” for lotteries, if the company can knock Belgium out of the park, how many other lotteries will choose Pollard given it can be a one stop shop, vs having to source suppliers for all of the functions Pollard will serve.

Meanwhile, Pollard has low leverage (under 2x 2025 EBITDA) and is family owned and operated. The Pollard brothers own ~64% of the company, and have never sold a share since it went public.

Pollard Banknote is trading under 10x free cash flow today, but that free cash flow is likely to fall off a cliff in 2028. That gives Pollard time to diversify its earnings away from NeoPollard more, to win more iLottery contracts, to replicate its success in Kansas in other states and countries. The charity and ticket printing businesses are both improving after an adverse legislative change (charity) and inflation induced margin compression (printing). Those businesses should keep growing sales and margins. And NeoPollard’s cash flows will be used to grow the other businesses.

It’s trading at ~12.5x EBITDA if you exclude all of NPI’s earnings, but adjust the enterprise value down by the $120 million I estimated as the net present value of NPI’s cash flows. That’s not dirt cheap, but that includes iLottery as a money loser, and with a few more contracts that multiple could come down pretty fast, and the multiple the company gets in the market could simultaneously increase quickly.

There are risks I’m thinking about. Traditionally, lottery spending has not been affected by economic downturns or recessions. Look at that chart of instant ticket sales above. Read this (or don’t since I just said what it says). People are always worried about the economy, but there’s a lot of data out there suggesting consumers are stretched, there’s a K shaped economy where the biggest lottery ticket buyers are hurting the most, etc. I’m not calling for a recession, but I will say that I have been scared out of buying good companies I like because I was worried about consumer spending (which has turned out to be a good call on Leon’s so far, though I’ve been considering it again).

Leon's Furniture

Before I start, I feel obligated to tell you that there are two very good writeups about Leon’s by better investors and writers than me.

While the relationship between the lottery and the economy has been true historically, that doesn’t mean it will be going forward.

Even more than that, I am worried about how sports betting and prediction markets will affect the lottery market. This paper found that in New York every $100 spent on sports betting results in $3.13 less spent on lottery tickets, and the introduction of mobile sports betting lowered weekly lottery sales by $11.5 million. This research found that lottery spending declines by 5% in the 16 months after online sports gambling begins in a territory, though this research found “sports betting does not impact overall monthly state lottery revenues,” so who knows. Logically though the gambler does not have unlimited dollars. They now have their choice of lottery, iLottery, online sports betting, iCasino, brick and mortar casinos, race tracks, and prediction markets, where they can bet on anything under the sun. There are probably other avenues for gambling that I’m missing, those were off the top of my head. It would not shock me if the gambler gets tapped out, and Pollard could suffer, particularly if it only does the instant tickets in a geography (vs having the iLottery contract as well).

I fear the effects of these things on Pollard, but I think the market has already feared them much more than I do.

Pollard stock has been a market darling before, reaching $60 in the mania that was 2021. If the charity and printing businesses can grow a bit, and Pollard wins a few more iLottery contracts, I think the market’s sun can shine on it again. In that scenario those multiples I used up there could easily be too low, or barring that, maybe the market will reward Pollard by valuing it at those multiples.

Some stocks are showing signs of the exuberance of 2021, but I doubt Pollard has a repeat of its run five years ago. At the time, Pollard was a play on people staying at home, doing more on the internet, etc. It was lightning in a bottle. Nobody is going to think of Pollard as a AI stock, or a data centre beneficiary, or even a commodity play if that takes hold. But Pollard has been beaten down enough that I think a few pieces of good news, could cause the sun to shine on it again.