Northwest Healthcare Properties REIT

Some day someone is going to write a fun case study on how different REITs performed over the 2019-2024 time period, and how their actions affected their returns. I’m not going to write that (yet?), but looking at Northwest Healthcare Properties REIT gave me the idea.

Let’s go back to the end of the year 2019.

Northwest returned 35% during the year, and had massively outperformed Canadian REITs over the past couple years. The unit price was a bit over $12, valuing it at ~15x FFO and over 90% of net asset value (NAV). It had a scarcity factor, as the only public entity in Canada by which to invest in healthcare real estate. Northwest had a portfolio of 175 properties in Canada, Germany, Netherlands, Brazil, Australia and New Zealand.

The REIT had debt of ~50% debt to gross book value ($2.7 billion of debt), in line with its target and down from 55% a year before. Debt to EBITDA was 9.8x. Interest coverage was 2.3x, and the REIT expected to bring leverage down to 42% and 8X EBITDA through a combination of equity raises and asset sales it had lined up. The weighted average interest rate (WAIR) on its debt was 3.89%, 72.2% of the debt was fixed rate, and 41% of the debt was maturing in 2022 (remember that, it will be important).

Debt was a bit high, though not outrageously so for a REIT (and investors could expect it to fall further), but the assets were very attractive and helped investors look past the debt.

Northwest had a weighted average lease term (WALT) of 14 years, geographic diversification, same property NOI growth over the last year of 2.2%, and occupancy over 97%. It also had an asset/property management arm that had grown AUM by over 100% in 2019. Combine all that with it being one of the only public ways to invest in its class of real estate and the 6.5% yield, it was no wonder that Northwest commanded a fair, if not high valuation in the market.

The REIT made it through 2020 very well. Rent collections were high, much higher than most commercial REITs, and the unit price ended 2020 almost exactly where it started the year. I was heavily invested in other real estate companies, so I can assure you that this certainly wasn’t the norm. It never cut its distribution, it acquired some more buildings, and at least vs book value, it deleveraged a bit (down to 48% LTV). FFO per unit increased a bit while NAV remained steady.

The results of Northwest during 2020 would have been the envy of many REITs.

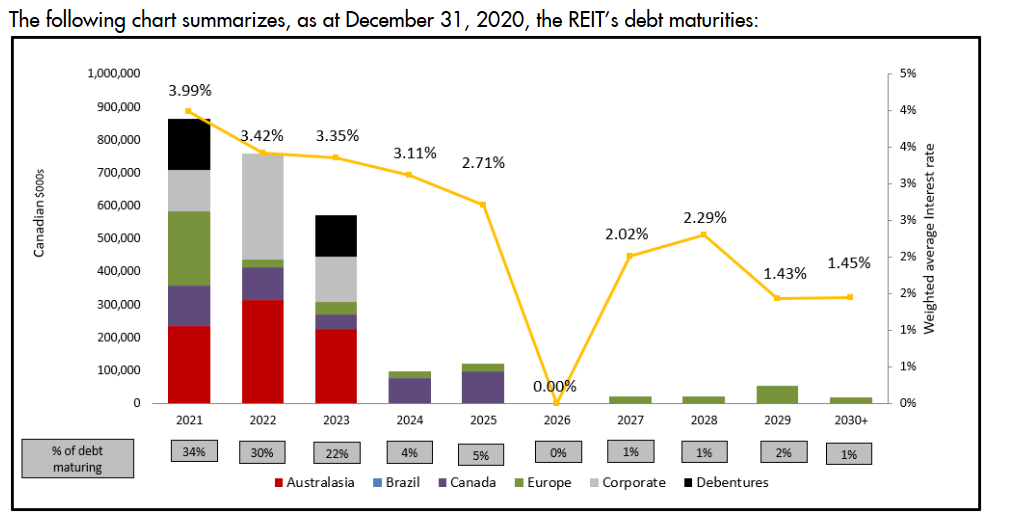

While LTV may have decreased to 48%, debt went up ~$60 million, and the proportion that was fixed rate dropped to 62.6%. Take a look at these two maturity graphs:

Northwest had under $400 million maturing in 2021 at the end of 2019.

It exited 2020 with almost $900 million maturing in 2021. It was able to reduce its weighted average interest rate down to 3.5%, but that came with the problem of refinancing.

2021 was more of the same. Fixed rate debt was down to 48.8%, while debt went up another ~$150 million, though by issuing a lot of units and some fair value gains, Northwest reported that debt was down to 42% LTV. The average interest rate on its debt was down all the way to 3.1%, and interest coverage was up to 3.37x. Alas, Northwest still had not solved its near term maturities:

Northwest entered the year with $1 billion (40% of its debt) to refinance. You’ll remember, from my last post, and just from living life, that 2022 was not a great year to be refinancing debt. Some REITs took the opportunity afforded by 2021’s rate environment to push out maturities and secure long term low rate debt. Northwest REIT chose a different path.

The REIT had rode the wave of low interest rates, and reached its peak of over $14 in March 2022, like all REITs. Even so, FFO per unit had hardly moved despite the tailwind of lowering interest rates, due to the REIT’s prolific issuance of units. FFO in 2018 was $99 million, while diluted units outstanding was 141 million, for FFO per diluted unit of $0.79. In 2021 was up to $178 million, but because units outstanding increased to 219 million, FFO per unit increased just 6% to $0.84.

Then the debt strategy caught up to it.

By the end of Q1 2022, debt had risen almost $300 million to $3.2 billion, fixed rate debt had fallen to 44% of the total, and WAIR had risen to 3.32%. After Q2 debt was over $3.7 billion, fixed rate was just 36% of debt, and WAIR was 3.77%. And still, Northwest had not bothered to push out any maturities:

In Q3, debt again increased to almost $4 billion, fixed rate ticked up to 40%, but WAIR was up to 4.61%.

After Q4, debt was up again to over $4.1 billion. During the year, debt had increased by over $1.2 billion despite units outstanding going up by another 20 million units. Despite units going up and fair value gains on its properties, all progress made on improving the balance sheet was lost as debt ended 2022 at 48.5% of assets and 11.7x EBITDA. Net operating income (NOI) increased by $59 million (up 20%), but interest expense went up by $60 million. Combine that with other income (management fees, interest income, etc) going down, and a few increased costs, and FFO ended the year down $10 million and FFO per unit fell to $0.70. WAIR ended the year at 5.35%.

Just when interest rates were exploding (I understand that’s hyperbole, but WAIR going up 72% in a year is a bit of an explosion), Northwest was investing $1.4 billion into its portfolio. It was up to 233 properties, from 175 three years earlier.

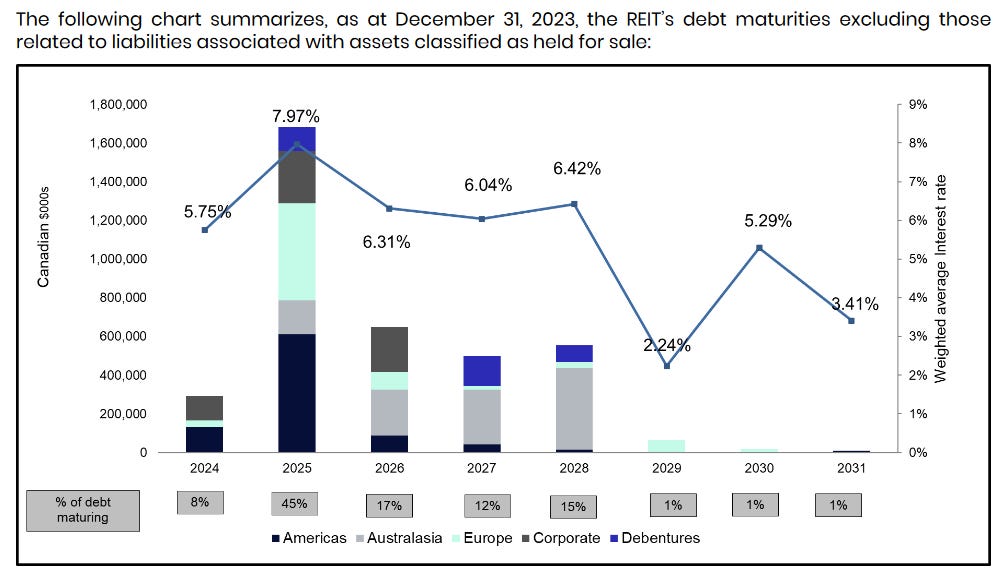

Shit hit the fan in 2022, but it wasn’t until 2023 that management realized it. I mean seriously, look at this debt maturity chart and tell me management is on the ball?

Early in 2023 management announced some non-core asset sales. It had previously announced it would joint venture (JV) its recently acquired UK assets, which would result in an influx of cash, and announced a new US JV. These would have made a huge difference for the balance sheet. Unfortunately the UK JV didn’t happen - Northwest announced it wasn’t happening on June 21st, after an update on May 12th about it progressing as planned (what I see as another example of the problems with management at the time).

In 2023 the CEO was ousted, the distribution was cut ($0.80 to $0.36), and the REIT got $360 million of proceeds from properties and $135 million from securities it sold. By the end of 2023 debt had actually gone down ~$170 million, and while the average interest rate had increased again to 6.8%, 70% of the debt was now at fixed rates. Most importantly though, the new CEO finally bought the company a little time by pushing maturities out:

It’s unfortunate that the new CEO Craig Mitchell took the helm when he did. The right move to reduce risk was to fix/hedge rates, but that of course was a huge hit to the financials and all that had to be done at punitive rates. Interest coverage dropped from a high of 3.37x in 2021 to 2.28x in 2022 and 1.88x in 2023, after interest increased $76 million from 2022’s already huge jump. FFO continued it’s precipitous fall, to $0.57 per unit.

Which leads us to today.

Craig Mitchell just announced he will be retiring in 2025, but his actions in 2024 show he doesn’t want to leave his successor with a mess like he inherited. So far this year, he has sold $1.2 billion of properties, including the UK assets his predecessor had purchased then tried to JV. He has hedged a lot of the debt and has a stated focus of pushing out maturities.

Q2’s FFO annualized is ~$0.36, however on the conference call management said that the sale of the UK assets would be $0.06 accretive in 2025 - the portfolio was sold at a 5.9% cap rate and the cash proceeds used to pay off debt with an average rate of 7.9% (along with retaining units of Assura PLC that it acquired in the deal, which pay an 8% distribution). Let’s call the current FFO run rate around $0.42.

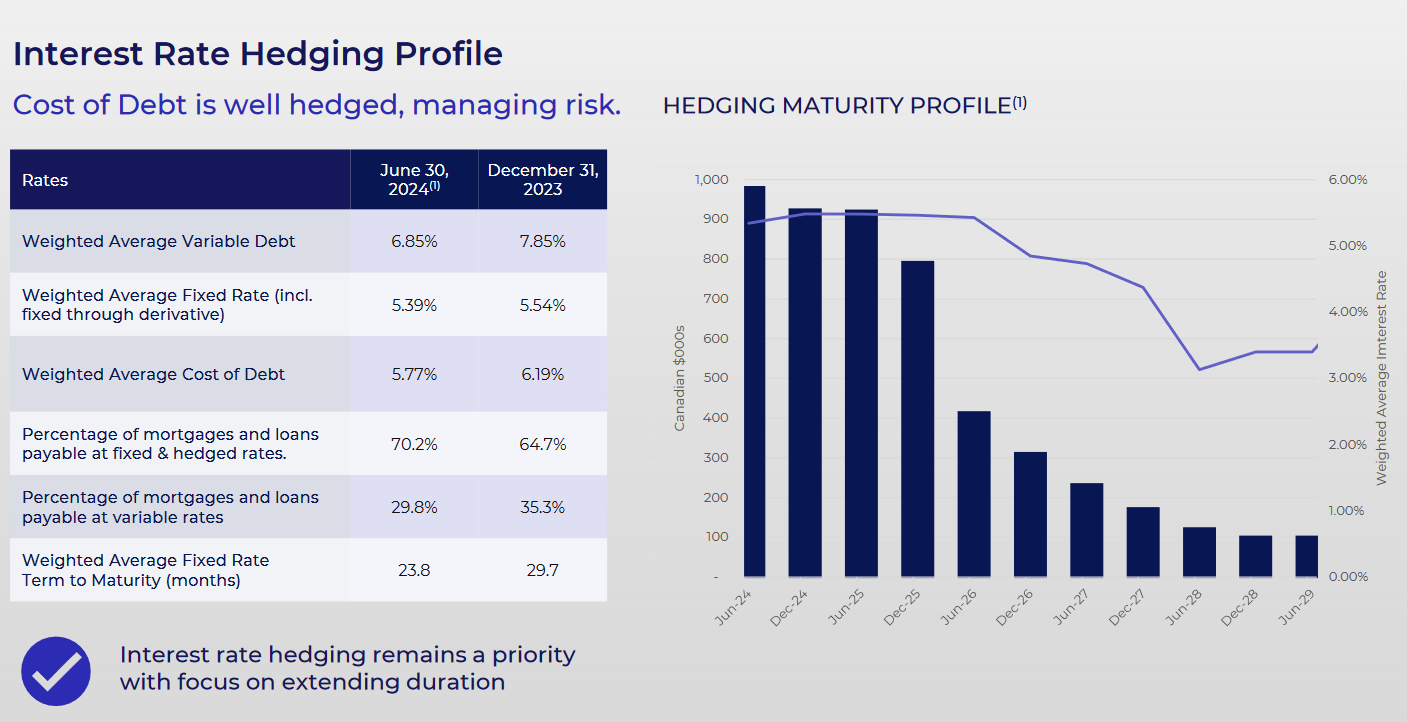

We also can clearly see just how much high interest debt Northwest has, that will be able to be paid off or refinanced in the near term. The UK sale was a large one, but was very accretive. Management knows it has a lot more high interest debt, and stated that it would be willing to sell assets opportunistically in order to pay down that debt… if it can be done accretively. Accordingly, the REIT recently announced it had another $200 million of assets listed for sale.

Even without further asset sales though, a lot of this debt should be able to be refinanced to push out maturities and/or reduce the rate.

Amongst Northwest’s debt, it has almost $900 million of debt that is at exorbitant rates, which any pay down of or refinancing will materially affect FFO.

Is it reasonable that the rates on this debt could be brought down to 8%? 7%? Any progress here is significant. For instance, the $125 million debenture I circled towards the bottom of the screenshot has a coupon of 10% and comes due in March 2025. Assuming that gets refinanced rather than paid down (the REIT announced the plan is to pay it off with its credit facility and proceeds from asset sales), every 1% drop in interest rates results in half a cent accretion to FFO. And that is just one small debenture amongst a whole pile of stinking debt. Lowering the rate on all the circled debt by 2% would result in $0.07 of additional FFO. Some of that is now done, seeing as the proceeds of the UK sale were used to pay off the highest interest variable rate debt - the WAIR on variable rate debt is down to 6.85% now - but there is still a lot of room to run.

Northwest has a very simple tailwind from rates dropping and refinancing its high interest debt. But what is it worth?

I admit that healthcare real estate is outside my wheelhouse, to the extent I have a wheelhouse. But real estate is real estate, and Northwest’s seems like it’s pretty good.

At the start of this post I mentioned the very long weighted average lease term in 2019. That remains the case today, with a WALT of 12.9 years. For comparison, Allied Properties REIT has a relatively long WALT at 5.9 years (it’s Northwest’s international properties that have the long lease terms, Canada’s WALT is 5.3 years). Occupancy has decreased… from 97% to 96.5%. Over 85% of its leases have rent escalators in them. Northwest has properties everywhere it had in 2019, along with the US now, and while it is tougher for me to analyze its international markets, it’s clear that Canada is actually dragging down a lot of the great metrics I’m referring to.

This is partly/mostly because the Canadian properties are medical office buildings, which as you can surmise, are very similar to office buildings, but with the benefit of being need based, mostly publicly funded tenants. The international assets include medical office buildings, but they’re a much smaller proportion of the assets. The rest of the international properties are hospitals, life sciences buildings, and the like. Those come with very different qualities/rent profiles, as you can see.

Anyone who has watched business news, or just news, or read stories online, or paid attention to stocks, or anything, in the last __ years can probably tell you a bull thesis for these properties.

“The population is getting older. As you get older you require more medical care….”

I could go on, but you really don’t need me for this. I don’t like to default to what a company is telling me, but Northwest does summarize the case nicely.

For the above reasons and more, I’m pretty comfortable suggesting Northwest’s properties are reasonably high quality and will remain in demand.

Northwest lists its NAV as ~$9.50 right now, when valuing its properties with an average cap rate of 6.22%. That doesn’t seem terribly off to me, but how the hell should I know whether 7.8% is a fair cap rate for a Brazilian hospital?

There is a lot going on right now - the UK portfolio sale, all the other assets and securities that have been sold, another $200 million of assets identified to be sold, all the debts at different rates being paid off, and whatever other actions management takes - that getting a real hold on the net asset value of its properties is probably beyond me. Until the portfolio is a little more stable, it seems fruitless to guess at a NOI number, let alone a cap rate and a value of its properties. Given the UK sale was done at a ~12% discount - though if you read between the lines on the conference call you can get the idea that there may have been slightly higher offers - let’s apply a 10% discount to the property values.

If you apply the loss from the UK sale and the 10% discount to all assets, you can get an adjusted book value of ~$4.40 per share.

You’ll notice two large adjustments to get from book value to NAV.

The deferred tax liability is an accounting convention, “the REIT has recorded deferred taxes in Europe, Brazil, and Australasia arising primarily due to the difference between the book value and tax cost of its investment properties”. There’s not much for me to say there. Adding this to our NAV brings it to ~$5.50, a touch higher than where Northwest trades today ($5.20 or so).

It’s the “global manager valuation adjustment” I want to touch on.

If you’ve been around for a while (I know there’s a handful of you), you’ll know that I love companies that earn fees managing assets for third parties while having a lot of their own invested capital. At one time I was tracking a basket of them, with the thesis they’d outperform the market from whatever starting point I had. That post and basket has been lost to time I’m afraid (I’m pretty sure it’s not outperforming however), but you can get a good idea of it from this twitter thread I did in 2022. I wasn’t aware that Northwest managed assets for others, or else I likely would have included it in that thread.

Currently the company earns fees for managing Vital Healthcare Properties Trust (a healthcare real estate trust publicly traded in New Zealand, which Northwest owns 28.5% of) and joint ventures of some of its properties.

Is $373 million the right valuation for this business? It seems a touch steep but not ridiculous. It’s likely to earn ~$40 million in fees this year. Dream Unlimited earned $25 million of FFO on $41 million of fee revenue in the first half of 2024. If Northwest had ~50% margins on its fee earning business, the valuation represents ~18x earnings/FFO for the asset manager. I think 50% margins could be high, and a 18x multiple is probably a little high considering the business has not been growing in the last few years. I will say that in 2019 the value Northwest assigned to the asset manager was $476 million, and two years ago it was over $500 million, so the current value on it has at least not been mindlessly propped up to mislead investors or inflate net asset value.

Keeping the value of the asset manager as is, we get to an adjusted NAV of ~$7.

Despite all of the problems and mishandling that I described above, before September 2023, Northwest was still trading over $6. All the signs were there that the distribution needed to be cut, but retail REIT investors are a special kind of optimistic, and waited to be told that it was cut before choosing to sell their units. Distributions, rightly, hold a special place in the heart of REIT investors, and it’s understandable that those who felt blindsided by the cut would not be in a hurry to own Northwest again.

The new lower distribution seems to be very sustainable. The run rate AFFO payout ratio is probably under 100% now, and will only improve going forward through any asset sales, debt paydown, or refinancings.

A Discussion About FFO and AFFO

I was reading a tweet thread the other day regarding Artis REIT, and one of the replies was from a smart guy, who I know knows REITs well (he follows me after all!), questioning why Artis REIT’s FFO (funds from operations) was so different from its AFFO (adjusted funds from operations).

Investing today, I don’t think one needs to worry about further distribution cuts. The current distribution is sustainable. I won’t speculate about when it might be increased - while I suspect that it would be possible to increase a couple cents by 2026 and maintain a sub 100% payout, I have no insight of whether that will be the REIT’s choice. Increasing the distribution may not be a priority in the near term, it wouldn’t shock me if Northwest chose further deleveraging, or to retain more cash to start growing again.

Back to the valuation, I personally like my adjusted NAV of $7. I think applying a 10% discount to the assets is sufficiently conservative.

If you trust the analysts at the big banks over me, I believe they range in their NAV estimates from $7.50 to $8.50. REITs are generally trading at discounts to analyst NAV estimates however, so you can apply a discount as you see fit. I could make a sensitivity table here, but I’m not looking to give you a target price or anything. A 25% discount (which would be on the larger side) on the analyst low estimate of $7.50 would be ~$5.60. A 10% discount (on the smaller side) would be $6.75. Those same discounts on the highest analyst NAV would be ~$6.35 and $7.65.

The current price represents 12.6x FFO, which doesn’t seem terribly cheap, but any REIT that trades at a similar valuation isn’t going to have the growth that Northwest is going to over the next couple years, and it probably isn’t going to have the high quality of Northwest’s portfolio. I don’t have a better multiple to suggest, nor do I have a good grasp on what FFO will be next year, I just know FFO will be higher, and that the FFO multiple seems like it could be low.

I threw a lot of numbers out there, but I’m confident that Northwest is undervalued. If forced to choose a target price, I’d say $6.50-$7. I think with a bit of positive news - debt is being paid down, the average interest rate on its debt is down, that it has sold more assets, etc - Northwest could trade up to that in the near future.

But if it doesn’t, you are going to own high quality real estate around the world, with needed tenants and an aging population that should keep demand for their services high, at a reasonable valuation vs cash flows. You’ll also collect a very sustainable 6.8% yield that can probably go up in the next few years. There are certainly worse consolation prizes.

A lot of publicly traded real estate companies and REITs have traded up in the past few months (though are working their way back down lately), making opportunities in the space harder to find. Northwest Healthcare Properties REIT seems like one of the better buys out there.

A final note, into addition to the convertible debenture that matures in March, Northwest has two more convertible debentures trading. NWH.DB.H matures in August 2027, and has a yield to maturity of 9.4%. It is convertible at $16, so that is very unlikely to be a kicker. NWH.DB.I matures in April 2028, has a yield to maturity of 9.6%, and is convertible at $10.55. Trading over $10.55 in 2028 seems possible from my perspective. But even if you don’t consider the conversion rights a benefit, this is pretty liquid debt that I think is mispriced given the REIT’s focus on paying down debt and how much safer the coupons are going to become. I think the units are a very good opportunity, but also that, for certain investors, these series of debentures probably offer a compelling value proposition.